Analysis | Read time: 7 minutes

The Gulf Cooperation Council (GCC) has entered an era of sharp economic division.

On one side stand Saudi Arabia, the United Arab Emirates, and Qatar, states backed by immense sovereign wealth that allows them to fund vast megaprojects and lengthy economic transitions.

On the other side stands Bahrain, a country facing an immediate and severe fiscal reality check.

As global oil prices face sustained downward pressure from weaker international demand and rising alternative energy production, the structural vulnerabilities of the region’s smallest economy have become clear. Bahrain has made notable progress in building a modern services economy, with non-oil sectors now generating 85 percent of its real gross domestic product (GDP).

However, its state budget remains deeply tied to hydrocarbon revenues. This dynamic has produced a widening structural budget deficit, exposing the sharp difference between successful economic diversification and actual fiscal self-sufficiency.

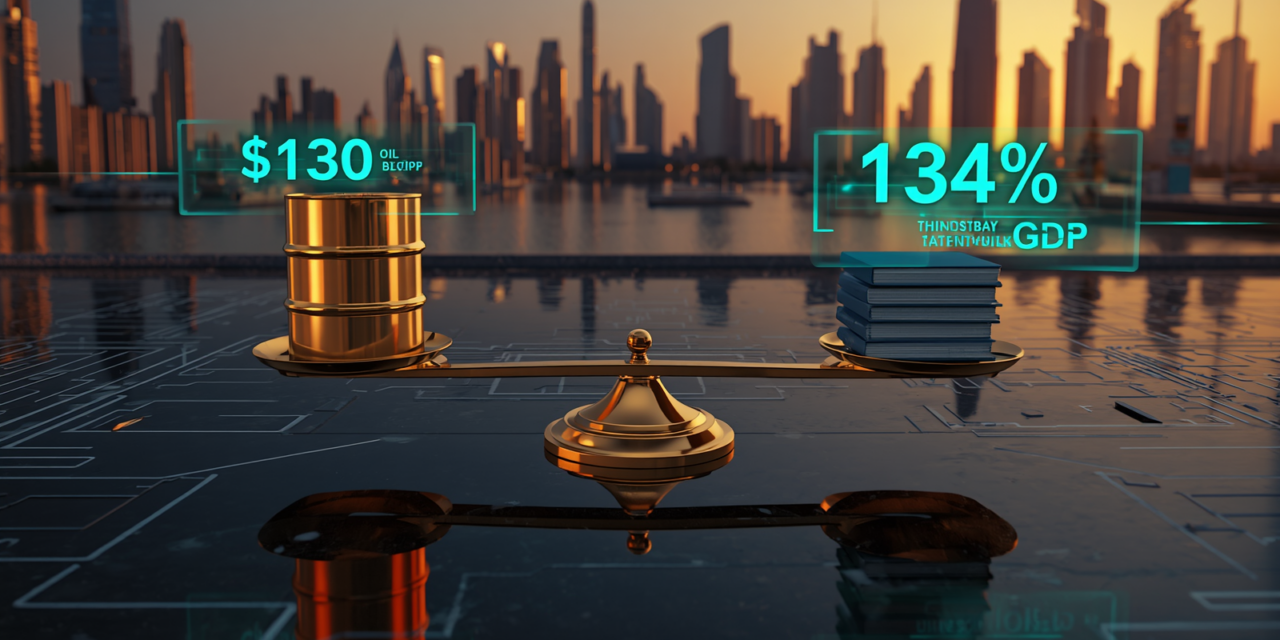

Bahrain’s Budget Requires $130 Oil to Break Even

The core of Bahrain’s economic challenge lies in a single, unyielding metric: the fiscal breakeven oil price. This is the price per barrel required to balance the state budget without drawing down reserves or taking on new loans.

According to data from the International Monetary Fund (IMF), Bahrain requires an oil price of approximately $130 per barrel to balance its budget [1]. With international oil prices expected to average around $70 per barrel through 2026, the structural shortfall is wide and persistent [2].

| Economic Indicator | 2024 Actual | 2025 Estimate | 2026 Projection |

|---|---|---|---|

| Fiscal Balance (% of GDP) | -11.0% | -10.8% | -10.2% |

| Government Gross Debt (% of GDP) | 134.0% | 131.1% | 139.7% |

| Non-Oil Sector Share of GDP | 82.1% | 85.0% | 86.4% |

| Government Overdraft at Central Bank | Peak level | Reduced by 8% | Facing renewed pressure |

Source: IMF Article IV Consultation, Bahrain, 2024 [1]

The figures show a clear trend. While neighboring Oman used the temporary oil price windfalls of recent years to reduce its public debt below 35 percent of GDP [3], Bahrain’s public debt has stayed high. The country’s debt-to-GDP ratio reached 131.1 percent in 2025 and is projected to rise toward 140 percent.

This heavy debt burden creates a compounding problem: escalating debt-servicing costs absorb a growing portion of government revenues, leaving fewer resources for productive public investment.

Bahrain Diversified Its Economy but Not Its Tax Base

For decades, Bahrain acted as a pioneer of economic diversification within the GCC. Long before regional neighbors launched their respective national visions, the kingdom developed a competitive financial services sector, built a large aluminum smelting industry through Aluminum Bahrain (Alba), and positioned itself as a regional logistics hub.

Today, financial services represent the single largest contributor to the economy at 17.8 percent of GDP, followed closely by manufacturing at 16.1 percent [1]. This successful transition of the real economy has not produced a stable, self-sustaining government budget.

The reason is structural. In Bahrain, non-oil activities generate 85 percent of national economic output, but hydrocarbon revenues still account for more than 60 percent of total government income [1]. This gap exists because the kingdom’s non-oil growth historically depended on low-tax regimes and generous state subsidies designed to attract foreign investment. The state absorbs the infrastructure and operational costs of maintaining a commercial hub, but it collects very little direct revenue from the wealth created within that hub.

When international oil revenues fall, the state budget suffers an immediate shock that the domestic commercial sector cannot offset.

A Refinery Attack Sharpened an Already Difficult Fiscal Picture

The urgency of this fiscal imbalance increased following geopolitical tensions in the Middle East during late 2024 and early 2025. The kingdom’s small geographic size and reliance on concentrated infrastructure make it particularly vulnerable to external disruptions.

An attack on infrastructure at the Sitra refinery, which processes domestic crude and oil imported via pipeline from Saudi Arabia for refining and export, disrupted energy production schedules and forced international economic agencies to revise their growth forecasts [4].

The IMF adjusted its 2026 economic outlook for Bahrain downward, projecting an overall economic contraction of 0.5 percent [1]. This revision reflects the combined effect of regional shipping disruptions in the Strait of Hormuz, rising insurance premiums for maritime trade, and unexpected infrastructure maintenance costs.

A 10% Corporate Tax Offers Revenue but Risks Competitiveness

To address this cycle, the Bahraini Cabinet approved a comprehensive fiscal reform package. The short-term goal is to generate an additional 1.1 percent of GDP in non-oil revenue through targeted fee adjustments and stricter expenditure controls [5].

The most significant shift is a legislative proposal to introduce a 10 percent corporate income tax, scheduled to take effect in 2027 [5]. This represents a major change for a country that built its reputation as a tax-free gateway to the Gulf.

The reform creates a direct policy trade-off. The state must urgently widen its tax base to pay down debt and reduce its reliance on emergency overdraft facilities at the Central Bank. At the same time, implementing corporate taxes and increasing administrative fees risks eroding the country’s primary competitive advantage.

Larger regional neighbors, such as Saudi Arabia and the UAE, offer massive domestic markets and multi-billion-dollar procurement contracts that attract multinational corporations even with corporate taxes in place. Bahrain’s domestic market is far smaller, meaning its primary appeal has always been the low cost of doing business. If fiscal consolidation measures raise corporate operating costs too high, foreign direct investment may shift to neighboring capitals.

Regional Support Now Comes with Conditions Attached

Bahrain’s fiscal management cannot be viewed separately from its political relationships. In 2018, Saudi Arabia, the UAE, and Kuwait provided a $10 billion fiscal balance program to support the kingdom through an earlier debt challenge [6]. This financial safety net stabilized the Bahraini dinar, which remains pegged to the US dollar, and reassured international bond markets.

The terms of regional financial support have since changed. Wealthier GCC states are currently engaged in their own expensive economic transformations. Saudi Arabia’s Vision 2030 project portfolio, for example, now demands sustained capital at a time when oil revenues are under pressure. These nations now expect their financial assistance to be paired with strict domestic fiscal discipline and concrete tax reforms. Regional capital is increasingly distributed as commercial investment rather than open-ended budgetary aid.

In response, Bahrain is reprioritizing its own Economic Vision 2030. Government fixed capital formation grew by 3.4 percent in 2024, but the focus has shifted away from prestige real estate projects toward infrastructure with direct economic returns [1]:

- Expanding transport links to handle higher volumes of regional trade

- Upgrading industrial zones to support high-value manufacturing and aluminum processing

- Modernizing digital infrastructure to expand cross-border financial and professional services

One concrete indicator of this pivot is the Central Bank of Bahrain’s 2024 open banking framework, which positions Bahrain as a regulated cross-border payments hub, an area where smaller financial centers can compete on regulatory quality rather than market size.

What This Means for GCC Executives

The ongoing fiscal adjustment in Bahrain carries significant practical consequences for corporate leaders, investors, and policymakers across the region.

Business models that depend on low-cost government inputs or permanent tax exemptions face clear structural risks. Executives must review their financial planning to account for higher regulatory fees, reduced utility subsidies, and the upcoming 10 percent corporate tax. Operational efficiency and market-driven value must replace tax optimization as the primary driver of corporate profitability in Bahrain.

The kingdom’s financial services and digital logistics sectors will remain central to its survival strategy. Because the state cannot match the industrial subsidies of its neighbors, Bahrain will likely focus on regulatory flexibility and specialized oversight to stay competitive. It is well-positioned to build depth in open banking, cross-border digital payments, and regional logistics management.

The widening economic divide within the GCC also means that a single, uniform approach to regional strategy is no longer effective. Companies operating across the Gulf must distinguish between the high-spending, project-driven markets of large oil exporters and the leaner, cost-conscious environment of Bahrain. Navigating this environment requires close alignment with the state’s specific development priorities and a clear understanding of where its fiscal reforms are heading.

The Harder Step in Diversification Is Still Ahead

Bahrain’s economic trajectory demonstrates that moving away from oil involves two distinct steps: diversifying commercial activities and restructuring state revenues. The kingdom completed the first step by building thriving financial, manufacturing, and tourism sectors. It is now working through the more difficult second step, aligning its government budget with that non-oil commercial reality.

The outcome of this effort matters beyond Bahrain’s borders. Small-state GCC economies that lack the hydrocarbon reserves of Saudi Arabia or the sovereign wealth of Abu Dhabi will eventually face the same structural question Bahrain is confronting today: how to fund a modern state when the oil revenue that built it begins to shrink.

The answers Bahrain finds, or fails to find, in the next three to five years will serve as a working reference for that wider problem.

Citations

[2] World Bank Commodity Markets Outlook. Commodity Price Forecasts, January 2025.

[4] Reuters. Bahrain refinery disruption forces energy output revision, February 2025.