Explainer | Read time: 10 minutes

Oman’s personal income tax, codified in Royal Decree No. 56/2025 and taking effect on January 1, 2028, makes the Sultanate the first GCC state to establish a comprehensive framework for taxing personal income [1].

The law is narrow by design: a high threshold, a single flat rate, and a set of exemptions that shield the vast majority of residents from any liability.

For senior expat professionals, corporate HR teams, and business owners, the years between now and 2028 are a preparation window, not a waiting period.

This article covers the full mechanics of the law, the exact rules that determine who owes tax and on what income, and the compliance obligations that fall on both individuals and their employers.

Why Oman Introduced a Personal Income Tax

Oman’s fiscal model has depended heavily on hydrocarbon revenue for decades. When oil prices fall, government budgets contract immediately [2]. Under Oman Vision 2040, the government set a target of raising non-oil revenue contributions to 15% of GDP by 2030 and 18% by 2040, and a personal income tax on top earners is one instrument in that plan [3].

The Oman Tax Authority has stated publicly that revenue generated from this tax will fund the national social protection system, infrastructure, and public services[1]. The government projects that approximately 99% of residents will owe nothing, which reflects how precisely the threshold has been calibrated to target only the highest earners[1].

The policy is not a response to a single year of low oil prices. It is a structural change, intended to give the Omani state a revenue source that does not move in lockstep with commodity markets.

The Threshold, the Rate, and Who Owes Tax

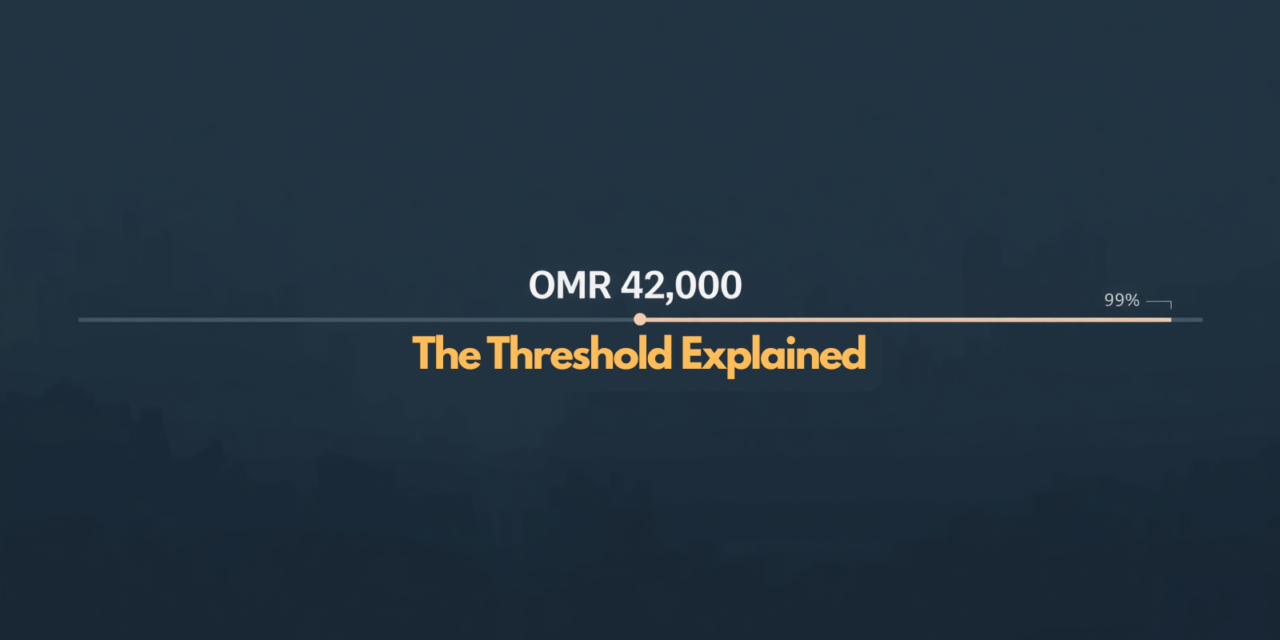

Tax liability begins only when a natural person’s gross annual income exceeds OMR 42,000, which is approximately USD 109,200 at current exchange rates[1]. Any income below that figure carries zero personal income tax liability. Above it, a flat rate of 5% applies to net taxable income, calculated after the threshold deduction and any allowable exemptions.

How the tax is calculated:

| Step | Description |

| 1. Start with gross income | Sum all taxable income categories across the year. |

| 2. Deduct the threshold | Subtract OMR 42,000 from gross income. |

| 3. Apply eligible deductions | Subtract approved items: education costs, healthcare, mortgage interest, zakat. |

| 4. Apply 5% rate | Multiply the remaining net taxable income by 0.05. |

Source: Royal Decree No. 56/2025, Oman Tax Authority. [1]

The law applies to both Omani nationals and foreign nationals. Nationality does not change the obligation. What changes the scope of taxable income is residency status.

Residency determines the scope of your tax liability

The law defines a tax resident as any individual who spends more than 183 days inside Oman during a single tax year, whether those days are consecutive or split across the year[1]. Tax residents are assessed on their worldwide taxable income. A non-resident, who spends fewer than 183 days in Oman, is taxed only on income earned or realized within Oman’s borders.

Eight Income Categories the Law Covers

The Oman Tax Authority has defined eight categories of earnings that individuals must aggregate to determine whether they cross the OMR 42,000 annual threshold[1].

These are:

- Employment earnings, including base salary, allowances, bonuses, and benefits provided in kind.

- Self-employment income from independent commercial activities, consultancies, or freelance services.

- Leasing and rental income from real estate or equipment.

- Royalties from intellectual property rights, patents, trademarks, or artistic designs.

- Investment and stock returns from corporate equities, bonds, and Islamic financial instruments (sukuk).

- Capital gains from the sale of corporate shares, stocks, or bonds.

- Real estate capital gains from the sale or transfer of property.

- Commercial interest from banking deposits, private lending, or corporate debt instruments.

Each of these streams adds to gross income for threshold purposes. An expat earning a base salary of OMR 38,000 who also collects OMR 6,000 in rental income from an overseas property is above the threshold and carries a tax liability on the excess.

Income That Is Legally Exempt from Tax

Royal Decree No. 56/2025 builds specific exclusions into the law to protect common income categories from tax liability[1].

The following are fully exempt from gross income calculations:

- Government retirement pensions and payments from recognized social insurance funds.

- End-of-service gratuities paid at the conclusion of an employment contract.

- Inheritance and gifts received through family succession, subject to regulatory validation.

- Salaries and allowances paid to accredited foreign diplomats and consular staff.

- Financial proceeds from selling an individual’s primary residential home.

Allowable deductions that reduce net taxable income

Taxpayers can also subtract specific personal expenditures from their gross income to reduce the taxable base[1].

Approved deduction categories include:

- Mandatory Islamic zakat payments and verified charitable donations to approved Omani organizations.

- Out-of-pocket healthcare costs and educational fees.

- Mortgage interest on a primary residence loan.

- For self-employment or rental income: either a flat deduction of 15% of gross income or actual documented operational expenses, with the method re-electable every three years.

What This Means for High-Earning Expats in Oman

For the 99% of Oman residents below the OMR 42,000 threshold, this law requires no action[1]. For senior expat professionals, the calculation is more involved.

The worldwide income rule is the most significant exposure

An expat who qualifies as a tax resident (183+ days in Oman) must declare global income, not just their Omani salary[1]. Rental income from a property in the UK, investment returns from a European brokerage, or freelance fees paid into an offshore account could all form part of gross income for Oman tax purposes.

The law provides a foreign tax credit mechanism. If an expat has already paid income tax on foreign-source earnings in another jurisdiction, Oman allows a credit against the Oman tax due on that same income[1]. This prevents dual taxation, provided the individual maintains accurate and dated documentation. The practical issue is that Oman has signed Double Taxation Treaties (DTTs) with a limited number of countries[4], so expats with assets in non-treaty jurisdictions should take legal advice before 2028.

Omanization compounds the compliance picture for employers

Expatriate hiring in Oman already operates within the constraints of Omanization, the Ministry of Labor’s policy of reserving certain technical, managerial, and administrative roles for Omani citizens[5].

From 2028, businesses recruiting senior foreign talent must also factor in whether an adjusted gross compensation package is needed to account for the 5% tax on earnings above OMR 42,000. A package that looked competitive before the law may require renegotiation.

Compliance Obligations for Employers and Institutions

Although the tax targets individuals, the law places withholding and reporting obligations directly on corporate entities[1].

Employers must track cumulative earnings across salaries, bonuses, and benefits to identify when an employee crosses the OMR 42,000 threshold. Once that threshold is crossed, the payroll system must calculate, withhold, and periodically remit the 5% tax to the Oman Tax Authority.

If an employee receives income solely from their salary, they may formally request their employer to file the annual tax return on their behalf[1].

For non-salary payments, separate rules apply. When a public or private organization pays out leasing fees, royalties, or share profits to a tax resident and the total exceeds OMR 20,000, the paying organization must withhold 20% of the tax due at source.

For non-residents, the full tax amount is deducted at the point of payment.

Key compliance timelines

| Compliance action | Statutory deadline |

| Annual filing | Electronic submission within 6 months of the tax year end. |

| Return revisions | Permitted up to 3 years from the original filing date. |

| Correcting errors | Mandatory revision within 30 days of discovering a data mismatch. |

| Audit window | Tax Authority may audit up to 3 years post-filing; 5 years in cases of fraud. |

| Late payment penalty | 1% additional tax per month accumulates on unpaid balances. |

Source: Royal Decree No. 56/2025, Oman Tax Authority. [1]

What Comes Next for GCC Fiscal Policy

Oman has demonstrated that a GCC state can introduce a personal income tax without triggering the talent exodus that regional governments have historically feared. The 183-day residency rule, the OMR 42,000 threshold, and the 5% flat rate together form a framework designed to be defensible internationally and manageable domestically.

The question the rest of the GCC will now watch closely is whether Oman’s 2028 data, the actual tax take, filing rates, and any shifts in expat hiring, shows the model working as intended.

If the revenue numbers hold and resident numbers do not fall, Bahrain, which carries the highest fiscal breakeven oil price in the GCC at a projected OMR 167 per barrel by 2030[2], will face a harder argument for indefinite exemption.

Oman has set a precedent. The 2028 enforcement date is not just a compliance deadline for businesses operating in Muscat. It is a data point the entire region is waiting to evaluate.