Investigation | Read time: 8 minutes

The physical conflict involving Israel, the United States, and Iran has forced Gulf Cooperation Council, GCC, sovereign wealth funds to rebuild their investment models.26

This escalation in 2026 caused a 94 percent decline in tanker traffic through the Strait of Hormuz.20 Rerouting costs and physical bottlenecks consumed much of the recent oil price peak of 114.97 dollars per barrel, so actual state revenues fell even as paper oil prices remained high.20

Budget planners measure financial health using fiscal breakeven prices, the oil cost per barrel that balances a state budget.27 Central government budgets often exclude off-budget capital spending by sovereign wealth funds, which creates a gap in official deficit reporting.20

Saudi Arabia’s direct government breakeven sits at 86.60 dollars per barrel, but consolidated costs exceed 94 dollars.20

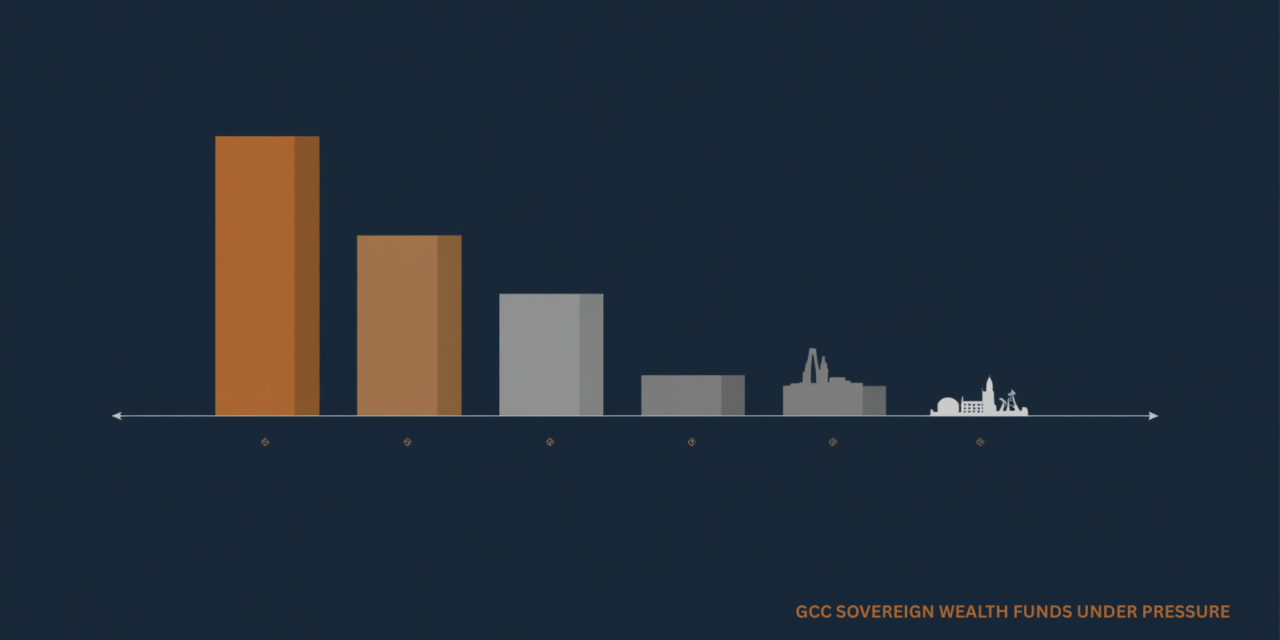

The table below outlines the primary financial pressures for each GCC nation in 2026.

| Nation | Fund | AUM (USD) | Breakeven | 2026 GDP | Primary pressure |

| Saudi Arabia | PIF | 900B | 86.60 | +4.5% | Giga-project commitments |

| Kuwait | KIA | 1.072T | 90.50 | -2.0% | Strait of Hormuz blockade |

| UAE | Mubadala | 385B | 65.00 | Under review | Global supply chain |

| Oman | OIA | 53B | 60.00 | +1.4% | Terms-of-trade adjustment |

| Bahrain | Mumtalakat | 18B | 130.00 | -0.5% | Sitra refinery disruption |

Sources: AUM figures from [3,5,7,14]; breakeven prices from [20,17,26,21,27]; GDP projections from [1,17,26,32,27]; pressure sources from [10,18,26,32,27].

Tight budgets force Saudi project cuts

The Public Investment Fund, PIF, which manages approximately 900 billion dollars, approved a minimum 20 percent spending reduction across its portfolio of more than 100 companies.2 Builders suspended work on the 170-kilometer mirrored linear city, The Line, and cut the 2030 target population from 1.5 million to under 300,000.20

The fund now concentrates resources on green hydrogen and commercially viable data center campuses that generate near-term yield rather than long-range prestige.20 This shift reflects a direct response to tighter oil revenues, not a change in the fund’s long-term diversification mandate.4

Aramco dividend shortfall strains state budget

Saudi Aramco must pay a base quarterly dividend of 21.89 billion dollars, but generated only 18.6 billion dollars in free cash flow during the first quarter of 2026.20 This gap forced Aramco to increase its gearing ratio, a metric comparing total debt to equity, by 26 percent to 4.8 percent in a single quarter.20

The Saudi government’s first-quarter deficit reached 33.5 billion dollars, which consumed 76 percent of the official full-year deficit target in ninety days.20

Both the government and the PIF depend heavily on Aramco dividend inflows, so the shortfall reduces the capital available for domestic project commitments simultaneously.20

Executive power resolves Kuwaiti gridlock

Kuwait’s Emir, Sheikh Meshal Al-Ahmed Al-Jaber Al-Sabah, dissolved the National Assembly to push fiscal reforms past years of legislative gridlock.28

In March 2025, the government enacted the Financing and Liquidity Law, which allowed the state to issue international bonds for the first time since 2017.29

This borrowing became critical after maritime blockades forced Kuwait Petroleum Corporation to declare force majeure, a legal clause that releases parties from contract obligations due to unavoidable events, on its oil exports.18 S&P projects a potential 2 percent contraction in Kuwait’s GDP for 2026.17

To stabilize the domestic economy, the Central Bank of Kuwait introduced ‘macroprudential policies’, regulations designed to protect the entire financial system rather than individual banks.30 These measures lowered liquidity requirements for local banks and allowed them to ease credit terms for war-affected customers.30

The Kuwait Investment Authority, managing 1.072 trillion dollars, provides the government’s primary financial buffer.5 The government plans to fund immediate structural deficits by drawing down assets from the General Reserve Fund.17

Global platforms shield Abu Dhabi wealth

Abu Dhabi’s Mubadala Investment Company reported that its assets under management reached 385 billion dollars by the end of 2025, driven by a five-year annualized return of 10.7 percent.7 The fund supports Abu Dhabi’s domestic non-oil economy through dedicated platforms including Aldar Capital for real estate and Mubadala Bio for biopharmaceutical capacity.8 S&P forecasts that Abu Dhabi could maintain a fiscal surplus averaging 3.8 percent of GDP through 2029.26

The Abu Dhabi crude pipeline to Fujairah bypasses the Strait of Hormuz entirely, allowing the state to export 50 percent of its crude directly to the Gulf of Oman.26

Mubadala’s global operations require careful management of geopolitical exposure.24 While the fund suspended new capital commitments in Russia in 2022, it retained stakes in existing projects there.24 At the same time, Mubadala continues active expansion in Western markets, including EQT’s acquisition of Intertek Group through Isotope Bidco in early 2026.25

This combination of domestic infrastructure advantage and diversified global exposure has insulated Abu Dhabi from the sharpest fiscal pressures affecting its GCC peers.26

Debt burdens expose deep fiscal divisions

The Oman Investment Authority recorded a profit of approximately 7.5 billion dollars in 2025, delivering an annual return of 14.6 percent.12 This performance allowed Oman to continue its debt-reduction program and cut its public debt-to-GDP ratio to 35.7 percent, down from a peak of 67.9 percent in 2020.21 Bahrain, by contrast, requires an oil price of 130 dollars per barrel to balance its state budget, the highest breakeven in the GCC.27

The IMF projects a potential 0.5 percent economic contraction for Bahrain in 2026 following infrastructure damage at the Sitra refinery.27

Bahrain’s public debt reached 131.1 percent of GDP in 2025.27 Standalone credit ratings for Mumtalakat, Bahrain’s sovereign fund, remain in the speculative BB category because its portfolio concentrates heavily on domestic assets.15

To address the fiscal shortfall, the Bahraini cabinet approved a reform package that cuts administrative expenses by 20 percent and introduces a 10 percent corporate tax in 2027.22 Mumtalakat also sold its entire holding in McLaren in April 2025 to improve portfolio liquidity.16

Co-investments shift the burden to private capital

Tightening fiscal conditions are prompting GCC rulers to move away from funding domestic developments unilaterally.2

Sovereign funds now structure platform-led co-investments that require foreign partners to contribute technology, expertise, and capital alongside the state.9 PIF’s platform companies, including Tasaru for mobility, Alat for advanced manufacturing, and Manara Minerals for mining, exemplify this model.4

Capital market reforms in Saudi Arabia now allow broader foreign investor participation in state project financing, reducing the direct draw on sovereign reserves.11

PIF’s decision to withdraw funding from LIV Golf signals a broader mandate shift away from prestige investments toward domestic sectors, including AI infrastructure, logistics, and mining, that generate measurable yield.10

Institutional investors and fund managers assessing GCC exposure should note that this shift concentrates sovereign capital in fewer, larger domestic platforms rather than spreading it across international portfolio positions.9 A portfolio heavily weighted toward PIF-linked vehicles now carries different concentration risk than it did in 2023, when international equity positions represented a larger share of AUM.19

Reviewing counterparty exposure to specific platform companies, rather than treating PIF as a single undifferentiated sovereign entity, is the practical step this transition demands.

A regional insurance pool could reduce shipping risk

Recent analysis of war-risk premium data indicates that escalating maritime insurance costs are compressing the trade balance across all five GCC states simultaneously.26

Regional policy advisors suggest that KIA, PIF, and Mubadala could collectively underwrite a joint cargo guarantee mechanism that insulates regional commercial corridors from external shock cycles.26 Such a structure would allow GCC states to set their own risk pricing for regional freight rather than accepting rates determined by London and New York insurance markets.26

No GCC state currently manages this risk at the sovereign fund level, which means the infrastructure to do so would require new inter-governmental coordination frameworks rather than a reallocation of existing fund mandates.

[1] vision2030.ai — Saudi GDP growth estimates.

[2] houseofsaud.com — PIF 20 percent budget cuts.

[3] Wikipedia — Public Investment Fund AUM.

[4] pif.gov.sa — PIF 2026-2030 strategy.

[5] Wikipedia — KIA 1.072 trillion AUM.

[7] mubadala.com — Mubadala AUM and returns.

[8] financemiddleeast.com — Aldar Capital and Mubadala Bio.

[9] twobirds.com — Platform-led co-investments.

[10] gulfif.org — LIV Golf withdrawal and NEOM scale-back.

[11] steptoe.com — Foreign ownership reforms.

[12] oia.gov.om — OIA 14.6 percent return.

[14] cfr.org — AUM table figures.

[15] spglobal.com — Mumtalakat standalone credit profile.

[16] fitchratings.com — Mumtalakat sale of McLaren.

[17] spglobal.com — Kuwait budget deficit and GRF drawdown.

[18] spglobal.com — Kuwait force majeure.

[19] fastcompanyme.com — PIF priority sectors.

[21] argaamplus.s3.amazonaws.com — Oman public debt to GDP.

[22] fitchratings.com — Bahrain administrative expense cuts.

[24] ridl.io — Mubadala Russian holdings.

[25] londonstockexchange.com — Mubadala Western expansion.

[26] spglobal.com — Abu Dhabi pipeline, fiscal surplus, war-risk context.

[27] thegccedge.com — Bahrain breakeven, GDP contraction, public debt.

[28] nbk.com — Kuwait Emir dissolving National Assembly.

[29] imf.org — Kuwait Financing and Liquidity Law.